Introduction

Buying a used car can save thousands of dollars compared to purchasing a new vehicle. However, financing plays a major role in the total amount you pay. Many buyers focus only on the monthly installment and forget about interest rates. That is why understanding what are used car loan rates is essential before signing any loan agreement.

Used car loan rates refer to the interest charged by lenders when you borrow money to purchase a pre-owned vehicle. These rates directly affect your monthly payment and the total loan cost. Even a small difference in interest can increase or reduce your expenses significantly over time.

Understanding What Are Used Car Loan Rates

Used car loan rates are the percentage of interest lenders charge on borrowed money for a used vehicle purchase. The interest rate determines how much extra you will pay besides the actual car price.

For example, if you borrow $15,000 for a used car with a 7% interest rate, you will repay the original amount plus the interest over the loan period. The longer the repayment term, the more interest you may pay overall. Unlike new car financing, used car loans usually come with slightly higher rates. Lenders consider used vehicles riskier because they depreciate faster and may require more repairs.

Why Used Car Loan Rates Are Higher Than New Car Rates

Many buyers wonder why used car financing costs more. The answer lies in lender risk. A new vehicle typically has a predictable market value and warranty coverage. On the other hand, a used car may lose value quickly or experience mechanical issues. Lenders also worry about older vehicles having lower resale value. If the borrower defaults, the lender may struggle to recover the remaining balance by selling the vehicle.

Additionally, used cars often have shorter loan terms. This increases monthly payments and affects how lenders structure interest rates.

Factors That Affect Used Car Loan Rates

Several important factors influence the rate you receive. Understanding them can help you qualify for better financing.

Credit Score

Your credit score is one of the biggest factors. Borrowers with excellent credit often receive lower rates because lenders view them as less risky.

People with poor or limited credit histories usually face higher rates. Therefore, improving your credit before applying can save money.

Loan Term Length

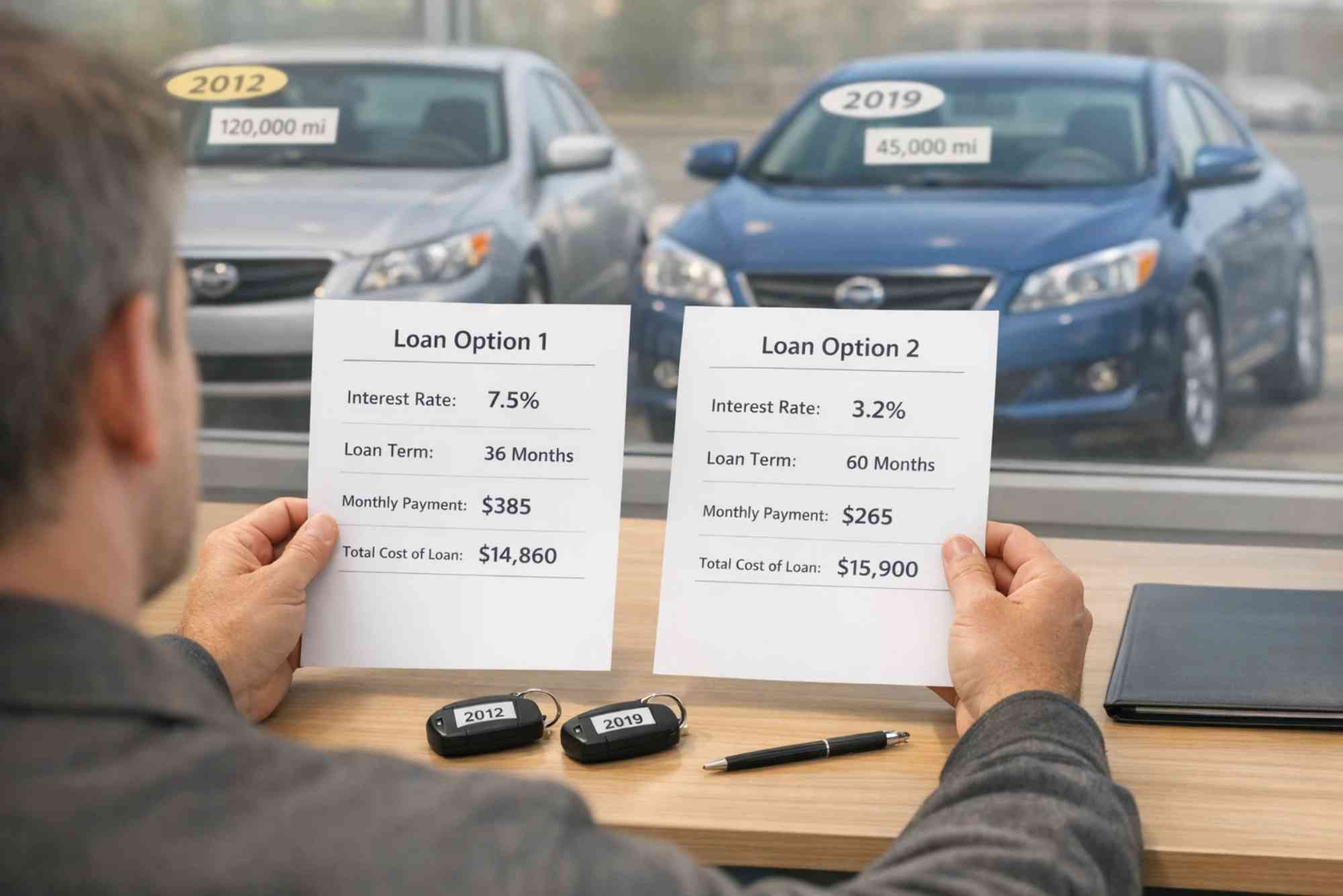

Shorter loan terms often come with lower interest rates. For instance, a three-year loan may have a lower rate than a seven-year loan.

Although longer terms reduce monthly payments, they increase total interest costs over time.

Vehicle Age and Mileage

Older vehicles or cars with high mileage often carry higher rates. Lenders worry these cars may lose value faster or break down sooner.

Newer used cars generally qualify for better financing terms.

Down Payment Amount

A larger down payment reduces the lender’s risk. As a result, borrowers who put more money upfront often receive lower interest rates.

It also reduces the total amount borrowed.

Income and Debt-to-Income Ratio

Lenders check whether your income can comfortably cover monthly payments. High existing debts may lead to higher interest rates or loan rejection.

Stable income improves approval chances.

Average Used Car Loan Rates in 2026

Average rates change depending on economic conditions and central bank policies. In 2026, used car loan rates typically range between 5% and 15%.

Borrowers with excellent credit may secure rates around 5% to 7%. Average credit scores often receive rates between 8% and 11%. Meanwhile, subprime borrowers may pay 12% or higher. Economic inflation and interest rate hikes also influence car financing costs. Therefore, comparing offers from multiple lenders remains important.

Where to Get the Best Used Car Loan Rates

Finding the right lender can make a huge difference in your financing costs. Several options are available today.

Banks

Traditional banks offer structured financing and competitive rates for qualified borrowers. Existing customers may receive loyalty discounts.

However, approval requirements can sometimes be strict.

Credit Unions

Credit unions often provide lower interest rates than banks. Since they are member-focused institutions, they may offer flexible terms.

Many buyers prefer credit unions for affordable used car financing.

Online Lenders

Online lenders have become increasingly popular. They allow borrowers to compare multiple offers quickly.

Some online lenders specialize in bad credit auto loans, making financing accessible to more buyers.

Dealership Financing

Car dealerships frequently arrange financing through partner lenders. While convenient, dealership loans may include higher markups.

Always compare dealership offers with outside lenders before making a final decision.

How to Get Lower Used Car Loan Rates

Securing a lower interest rate can save hundreds or even thousands of dollars. Fortunately, there are several ways to improve your chances.

Improve Your Credit Score

Pay bills on time and reduce outstanding debt before applying for a loan. Even a small improvement in credit score can lower rates.

Checking your credit report for errors is also important.

Make a Larger Down Payment

A bigger down payment reduces the loan amount and lender risk. Consequently, lenders may reward you with better rates.

It also lowers monthly payments.

Compare Multiple Loan Offers

Never accept the first financing offer you receive. Instead, compare rates from banks, credit unions, and online lenders.

Shopping around increases the chances of finding better terms.

Choose a Shorter Loan Term

Short-term loans usually have lower rates. Although monthly payments may be higher, overall interest costs decrease.

This option works well for buyers with stable income.

Get Pre-Approved

Loan pre-approval helps buyers understand their budget before shopping for a car. It also strengthens negotiating power at dealerships.

Many lenders offer free pre-approval applications online.

Fixed vs Variable Used Car Loan Rates

Used car loans generally come with either fixed or variable interest rates.

A fixed rate remains the same throughout the loan term. This means monthly payments stay predictable. Most borrowers prefer fixed-rate loans because budgeting becomes easier. A variable rate can change over time depending on market conditions. Initially, these loans may offer lower rates. However, payments can increase later if interest rates rise.

For long-term financial stability, fixed rates are often safer.

How Used Car Loan Rates Affect Monthly Payments

Interest rates directly impact monthly installments. Higher rates increase the amount paid each month and the total loan cost.

For example, borrowing $20,000 for five years at 6% costs much less than borrowing the same amount at 12%.

Even a few percentage points can significantly affect affordability. Therefore, buyers should calculate total repayment costs, not just monthly payments.

Common Mistakes Buyers Make With Used Car Loans

Many people make avoidable mistakes during financing. Understanding these errors can help you avoid unnecessary costs. One common mistake is focusing only on monthly payments. Dealers may extend loan terms to lower payments while increasing total interest. Another mistake is skipping loan comparisons. Accepting the first offer can result in higher rates.

Some buyers also ignore additional costs such as taxes, registration fees, and extended warranties. Finally, failing to read loan terms carefully can create financial surprises later.

Should You Refinance a Used Car Loan?

Refinancing can help borrowers secure lower interest rates after improving their credit scores or financial situation. For example, if rates drop or your credit improves significantly, refinancing may reduce monthly payments and overall costs.

However, refinancing works best when the loan balance remains high enough to justify fees or administrative costs. Before refinancing, compare savings carefully.

Tips for First-Time Used Car Buyers

First-time buyers should create a realistic budget before shopping. Consider insurance, fuel, maintenance, and registration costs in addition to loan payments. It is also wise to research vehicle reliability and resale value. A cheaper car with high repair costs may become expensive later.

Always review the vehicle history report and get a mechanical inspection before purchasing. Most importantly, understand what are used car loan rates before agreeing to financing terms.

Conclusion

Understanding what are used car loan rates is crucial for anyone planning to finance a pre-owned vehicle. Interest rates determine how much you pay over the life of the loan, making them one of the most important parts of the buying process. Several factors affect rates, including credit score, loan term, vehicle age, and down payment amount. Fortunately, buyers can improve their chances of securing lower rates by comparing lenders, improving credit, and choosing shorter loan terms.

This article explores whether Etoro is good for long term investment, analyzing fees, risks, and portfolio diversification options. Investors should understand market volatility and platform features before committing funds. For more details, click the internal link using anchor text: Is Etoro Good for Long Term Investment? It helps readers evaluate risks before investing online. Always do research.

FAQs

What are used car loan rates based on?

Used car loan rates are based on factors such as credit score, income, loan term, down payment, and the vehicle’s age and mileage.

What is a good interest rate for a used car loan?

A good used car loan rate usually falls between 5% and 7% for borrowers with excellent credit scores.

Can I get a used car loan with bad credit?

Yes, many lenders offer financing for bad credit borrowers. However, the interest rates are typically higher.

Do used car loan rates change frequently?

Yes, rates can change depending on economic conditions, inflation, and central bank interest rate policies.

How can I lower my used car loan rate?

You can lower your rate by improving your credit score, making a larger down payment, comparing lenders, and selecting a shorter loan term.

Is dealership financing good for used cars?

Dealership financing can be convenient, but buyers should compare outside lenders to ensure they receive competitive rates.